Variance analysis

By the end of this session you will be able to:

- Compare budgeted cash flows and actual cash flows

- Determine variance analysis

In this session you will be looking at variance analysis.

- The subject is about comparing the cash budget data with the actual data to determine the amount of differences that exist.

- The process acts as a monitoring and controlling tool to inform management of any major issues.

- If there are major variances (differences) the management board will want to know the causes by requesting the Accountant to investigate and to rectify those issues within their control.

- For example, if material prices are high, then change the supplier to obtain a better deal on prices.

- However, there are items that the organisation will not be able to control such as interest rates and exchange rates.

- These are external factors outside the control of the organisation’s accountant.

Prepare a short Power Point to present your answer for the task below:

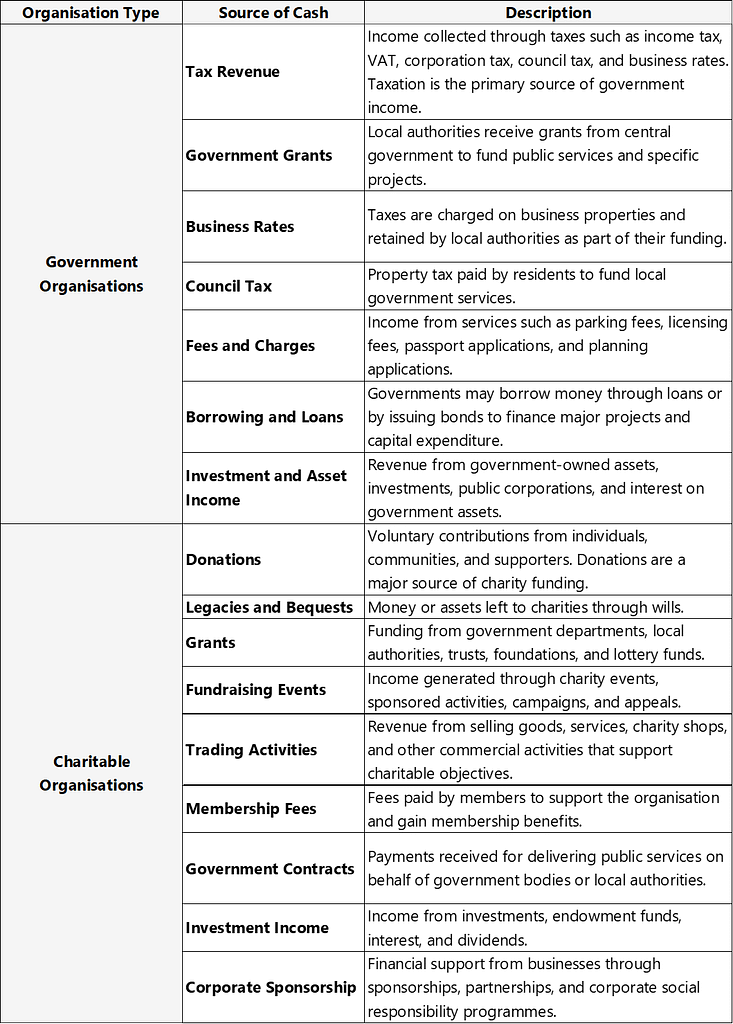

The cash budget is important to business entities but it is also useful for other organisations. Carry out research to find out the sources of cash that can be found in government and charitable organisations.

Have a look at the postings made by your colleagues to the discussion forum and comment on at least two other postings.

Some of the things you may wish to think about when you are studying other postings include:

• Do any of your colleagues share the same understanding of the topic?

• What do you think of the sources of cash they have selected?

• How do they compare to your sources of cash you selected?

Padlet password: 12345

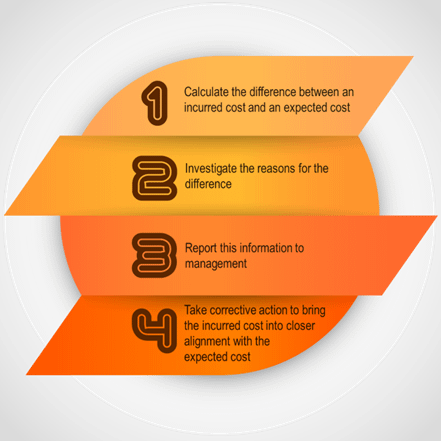

Cost variance analysis is a control system that is designed to detect and correct variances from expected levels. It is comprised of the following steps:

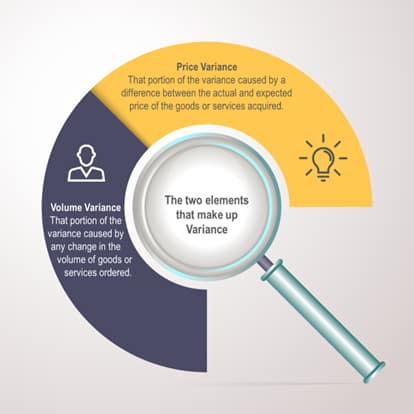

The simplest form of cost variance analysis is to subtract the budgeted or standard cost from the actual incurred cost, and reporting on the reasons for the difference. A more refined approach is to split this difference into two elements:

A standard costing system consists of two elements

- For example

- A company has an unfavourable variance in its cost of goods sold of £80,000.

- A detailed cost variance analysis reveals that the company sold several hundred more units than it expected, and the cost of those additional units comprised £70,000 of the variance.

- This was hardly indicative of poor performance, since it implied that the company was selling more units.

- Only the remaining £10,000 of the unfavourable variance was due to unusually high prices, which could then be investigated in detail.

- Thus, it frequently makes sense to divide cost variance analysis into price and volume variances, thereby gaining better insights into the costs incurred.

- The following worked example will help you to see how variance analysis is used in a practical situation via worked example.

- In addition, the demonstration allows you to familiarise yourself with how questions will need to be answered.

- Once you have studied the worked example please attempt the accompanying activity.

- Before we start let us just refresh our understanding of variance.

- In budgeting, a variance is the difference between a budgeted cost and the actual amount incurred. It is worth noting that variances can be calculated for both costs and revenues.

- A standard costing system consists of the following four elements:

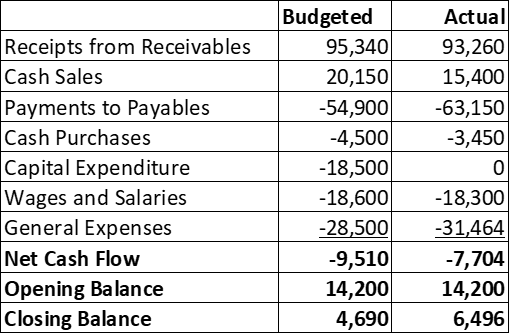

Mica Ltd is a small company and you have been asked to prepare its quarterly budget to 30 September 2020. The quarterly budgeted and actual data for Mica Ltd are shown below.

Budgeted Actual

Receipts from receivables 97,268 93,084

Cash sales 16,885 18,469

Payments to payables -46,880 -49,270

Cash purchases -8,360 -8,195

Capital expenditure 0 -35,200

Wages and salaries -20,020 -20,460

General expenses -26,950 -24,710

Net cash flow 11,943 -26,282

Opening balance 4,620 4,620

Closing balance 16,563 -21,662

Required

a) Prepare a reconciliation statement of the budgeted cash closing balance with the actual closing cash balance

b) From the options below, choose which action best suits the business to take in order to avoid an overdrawn from the bank:

- Chased customers to settle their accounts earlier

- Discuss with suppliers an extended credit term

- Increased cash sales by offering discounts

- Postpone the purchase of capital expenditure

- Negotiate and agree lower wages payments to staff

c) Match each cause of variance listed below with one of the following possible courses of action.

- Better credit control

- Alternative suppliers

- Reduce overtime working

- Negotiate early settlement discount

- Increase the usefulness of the product

Variances:

- Labour costs have increased

- Sales volume have decreased

- Payments to suppliers are being made earlier

- Customers are taking more days to settle their debts

- Prices of raw materials have increased

- This activity is an important part of your learning and will help you to test your understanding and reinforce what we have just covered.

- Use a spreadsheet, (like Microsoft Excel) to attempt the activity and remember to save it with a meaningful name, somewhere you can easily find it. Alternatively, you could do all of your work using a pen and paper, photograph it using your mobile and save it on your computer as an image file.

- Once you have completed the question please click on the ‘Check your answer’ link and compare your answer to the worked solution. This step is very important because it will also enable you to understand where you may have gone wrong and to make sure that you do not make the same mistake again.

- If after looking at the solution, you still do not understand where you may have gone wrong, please post a question on the discussion forum for further assistance. Remember, to include your answer with your posting.

The quarterly budgeted and actual data for an organisation are shown below.

Required

- Prepare a reconciliation statement of the budgeted cash closing balance with the actual closing cash balance

- Match each cause of variance listed below with one of the following possible courses of action

- Improve credit control

- Ensure available credit is being taken

- Increase labour efficiency

- Change suppliers

- Provide salespeople with incentives

Variances:

- Labour costs have increased

- Sales volume has decreased

- Payments to suppliers are being made earlier

- Customers are taking more days to settle their debts

- Prices of raw materials have increased

Please complete this short questionnaire.

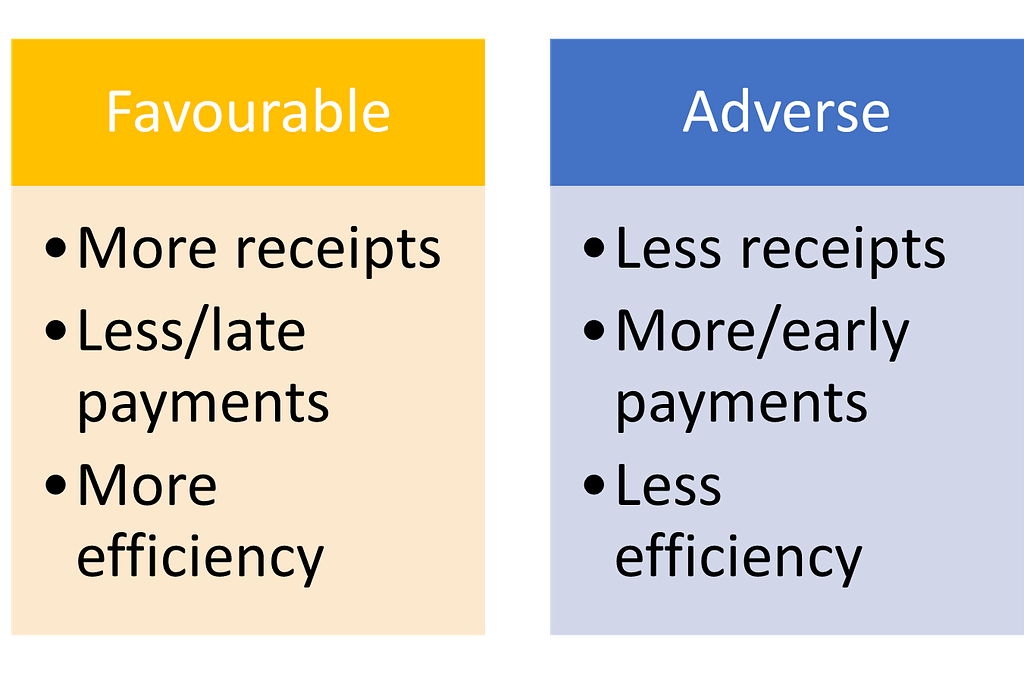

- In this session you considered another financial tool in variance analysis to enable the accountant to compare the cash budget figures with actual figures to determine whether an adverse or favourable variance has occurred.

- This tool is use for monitor and control purposes to enable management to correct items it has control over and to minimise those items such as increase prices through inflation it has no control of.

- To reinforce the subject matter, we recommend that you go through the course pages again in preparation for your 2nd assignment.

- In the next session, you will consider the working capital cycle.