Financial Markets & Regulation: The Prudential Regulation Authority (PRA)’s Approach to Small Insurers

By the end of this session, you should be able to understand the approach of The PRA to Supervision for Smaller Insurers

- Prepare a video (a PowerPoint file with sound and export it to a video format. Then, upload it to Padlet)

- How many firm categorisations are there under the PRA supervision?

- What is The Prudential Regulation Authority (PRA)’s Approach to Supervision for Small Insurers?

- The PRA’s statutory objectives:

- General objective:

“promoting the safety and soundness of PRA-authorised firms” - Insurance objective:

“contributing to the securing of an appropriate degree of protection for those who are or may become policyholders”

- General objective:

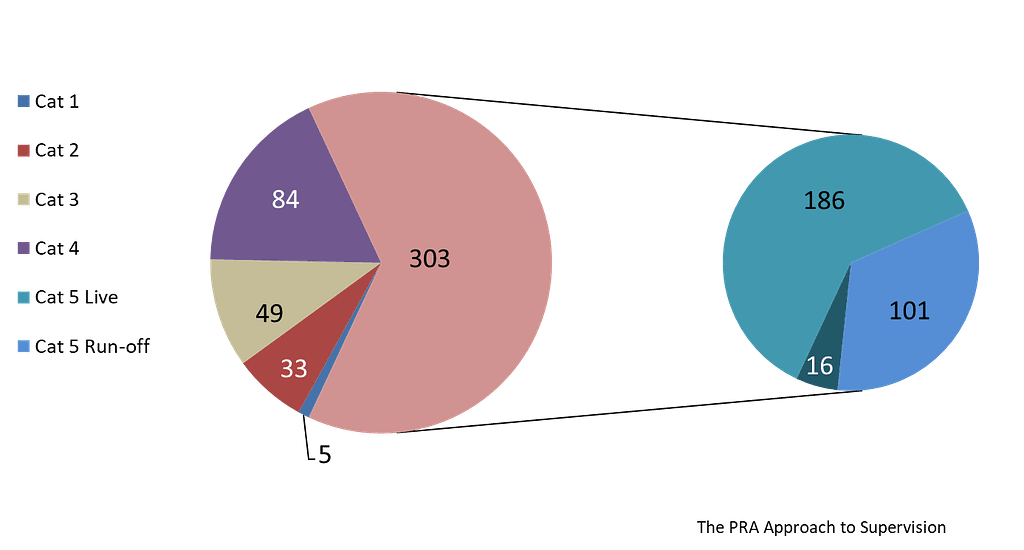

Five ‘categories’

- A core part of the risk assessment is the potential impact assessment.

- The PRA assess the significance of a firm to the stability of the UK financial system.

- This ‘potential impact’ reflects a firm’s potential to affect adversely the stability of the system by failing, coming under operational or financial stress, or because of the way in which it carries out its business.

Five ‘categories’ – Explanation

Divide all deposit-takers and designated investment firms that PRA supervise into the five ‘categories’ of impact below:

| Category 1 | The most significant deposit-takers or designated investment firms whose size, interconnectedness, complexity, and business type give them the capacity to cause very significant disruption to the UK financial system (and through that to economic activity more widely) by failing, or by carrying on their business in an unsafe manner. |

| Category 2 | Significant deposit-takers or designated investment firms whose size, interconnectedness, complexity, and business type give them the capacity to cause some disruption to the UK financial system (and through that to economic activity more widely) by failing, or by carrying on their business in an unsafe manner. |

| Category 3 | Deposit-takers or designated investment firms whose size, interconnectedness, complexity, and business type give them the capacity to cause minor disruption to the UK financial system by failing, or by carrying on their business in an unsafe manner, but where difficulties across a whole sector or subsector have the potential to generate disruption. |

| Category 4 | Deposit-takers or designated investment firms whose size, interconnectedness, complexity, and business type give them very little capacity individually to cause disruption to the UK financial system by failing, or by carrying on their business in an unsafe manner, but where difficulties across a whole sector or subsector have the potential to generate disruption. |

| Category 5 | Deposit-takers or designated investment firms whose size, interconnectedness, complexity, and business type give them almost no capacity individually to cause disruption to the UK financial system by failing, or by carrying on their business in an unsafe manner, but where difficulties across a whole sector or subsector may have the potential to generate some disruption. |

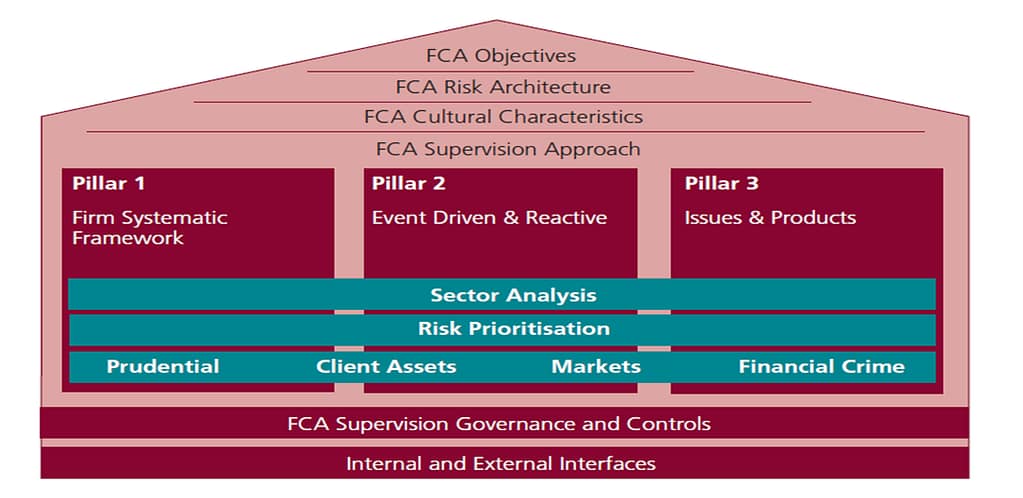

Significant firms & Supervisory Models

- Significant firms: categories 1 & 2 and smaller firms: categories 3-5

- Supervisory Models

- Category 4 firms:

- The annual supervisory assessment visit

- Desk-based reviews of returns and management information

- Issue-driven meetings and reactive work

- Peer group and trend analysis

- Category 5 firms:

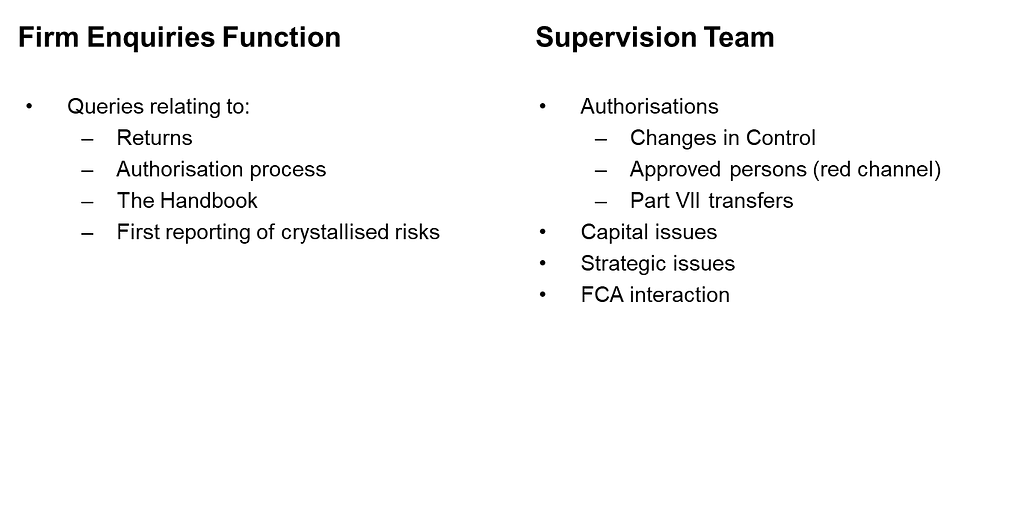

- Firm enquiries function for routine queries

- Broadly reactive supervision in response to crystallised risks

- Some proactive analysis and assessment at solo and peer-group level

- Category 4 firms:

Read more:

Activity

What is The PRA Approach to Supervision? “Forward-looking and judgement-based supervision…” What does this mean in practice?

Three key principles

The PRA’s supervisory approach follows three key principles:

- judgement-based

- Judgement-based supervision is presented as a new approach to the way financial institutions are supervised. As such it addresses the how-to supervise, rather than the what or the who

- The essence of a judgement-based approach is a willingness to intervene when the regulator judges that the outcomes will, in future, be at variance to its mandate, even if the firm does not agree.

- Such proactive intervention needs to be proportionate and justified, but if we are to improve outcomes and meet the expectations of Parliament and society, such judgements will have to be made.

- forward-looking

- Assess insurers not just against current risks, but also against those that could plausibly arise in the future.

- Where the PRA judge it necessary to intervene, they generally aim to do so at an early stage.

- Insurers should be open and straightforward in their dealings with PRA, taking the initiative to raise issues of possible prudential concern at an early stage.

- PRA will respond proportionately.

- In this way, trust can be fostered on both sides.

- Risk monitoring and risk control entail a great deal of judgment. Various supervisory tools (reports and statistical requirements),

- internal ratings (CAMELS – Capital adequacy, Asset quality, Management, Earnings, Liquidity and Sensitivity to Market Risk and others),

- on-site examinations,

- internal audits,

- off-site examinations,

- consultations with senior management and others (disclosure, fiduciary duties) require that supervisors exercise forward-looking judgement.

- It is as much an art as science.

- focused on key risks.

- focus the supervision on those issues and those firms that, in their judgement, pose the greatest risk to the stability of the UK financial system and, in the case of insurers, to policyholder protection.

Firm Enquiries & Supervision Team

Transfers of insurance business

Transfers of insurance business under Part VII of the Financial Services and Markets Act 2000

- An insurance business transfer scheme is defined in section 105 of FSMA and the definition has been extended to transfers from underwriting members and former members of Lloyd’s.

- The business transferred may include liabilities and potential liabilities on expired policies, liabilities on current policies and liabilities on contracts to be written in the period until the transfer takes effect.

- The parties to schemes approved under foreign legislation or involving novations of reinsurance or a captive insurer can apply to the court for an order sanctioning the scheme.

- The parties (usually insurers and transferees) may apply to the High Court.The court reviews:

- fairness

- impact on policyholders

- regulatory compliance

- If satisfied, the court sanctions (approves) the scheme.

- This gives the transfer full legal effect.

- The parties (usually insurers and transferees) may apply to the High Court.The court reviews:

- The PRA is likely to consider a novation or a number of novations as amounting to an insurance business transfer only if their number or value were such that the novation was to be regarded as a transfer of part of the business.

- A novation is an agreement between the policyholder and two insurers whereby a contract with one insurer is replaced by a contract with the other

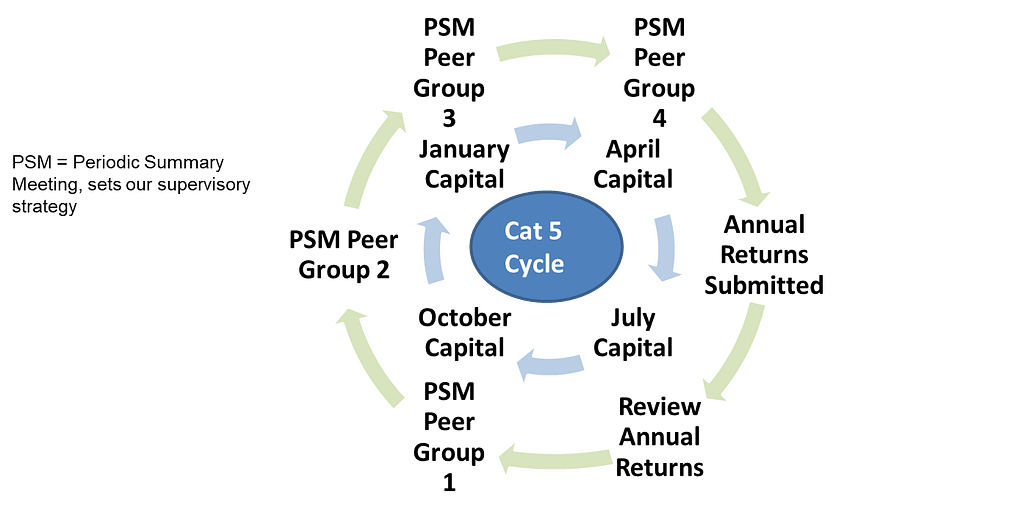

Periodic Summary

Threshold Conditions

- Threshold Conditions

- Minimum requirements that firms must meet at all times in order to be permitted to carry out regulated activities

- Firms will need to meet both PRA-specific and FCA-specific threshold conditions

- PRA-specific threshold conditions:

- Legal status

- Location of offices

- Prudent conduct

- financially sound

- managed safely and responsibly

- able to meet liabilities as they fall due

- compliant with prudential standards (e.g., solvency requirements)

- Suitability

- This focuses on the people who run the firm. The FCA/PRA expect:

- directors and senior managers to be fit and proper,

- honest, competent, and financially sound,

- governance arrangements to be appropriate,

- the firm to treat customers fairly.

- This focuses on the people who run the firm. The FCA/PRA expect:

- Effective supervision

- The PRA will assess firms against the threshold conditions on a continuous basis

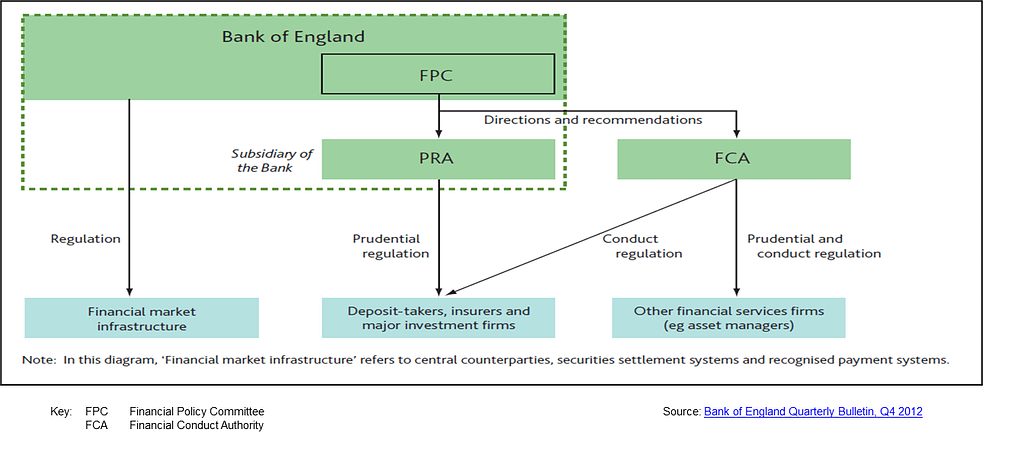

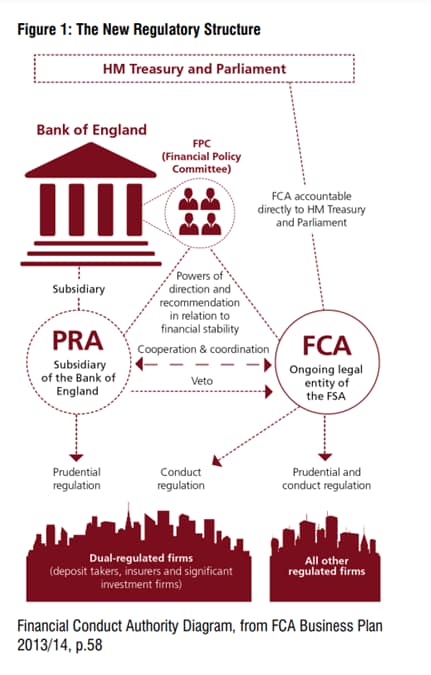

- Effective delivery of PRA’s approach requires coordination with the FCA

- Focussed at the firm level

- MoU (Memorandum of Understanding) and colleges to ensure statutory duty to co-ordinate is effective

- Firm-specific supervision alone is not sufficient to deliver financial stability.

- Must be complemented by an effective macroprudential regime.

- The two-way flow of information and exchange of views between the PRA and the FPC (Financial Policy Committee)

- PRA is responsible for implementing relevant FPC recommendations on a ‘comply or explain’ basis

- FPC has powers to direct the PRA

- Their main objectives are to:

- Communicate the PRA objectives and expectations to the industry clearly.

- Understand market trends in order to inform their forward-looking approach and communicate supervisory priorities for the sector.

- Raise awareness of the information and support available to smaller insurers.

Activity: Identify the risks that insurers may face, the impact of these risks and suggest solutions

- An emerging risk can be defined as:

- “an issue that is perceived to be potentially significant but which may not be fully understood or allowed for in insurance terms and conditions, pricing, reserving or capital setting”. (Source: Lloyd’s of London)

- Examples:

- Artificial intelligence risks

- Climate change patterns

- New diseases (pandemics)

- Cyber threats

- Changes in social behaviour or legal trends

- This means the risk is:

- New, evolving or unfamiliar

- Lacking in historical data

- Difficult to model or predict

- It means insurers may not yet have:

- ✔ Policy wording

- The risk might not be clearly addressed or excluded in current insurance contracts.

- ✔ Pricing models

- Premiums may not reflect the real cost of the risk because it is not well understood.

- ✔ Reserves

- Insurers may not have set aside enough money to pay potential claims.

- ✔ Capital requirements

- Regulatory capital may not fully account for that new or emerging exposure.

- The key drivers of risk include:

- Economic, technological, environmental and socio-political developments as well as the interdependencies between them.

- Other risk drivers can include:

- The changing business environment such as liability issues, evolving regulatory regimes, stakeholder expectations, and shifts in risk perception.

- This session will concentrate on the insurable areas of risk for both life and general insurers.

- These risks include:

- Life Products Risk

- credit & counterparties, impact of the low-interest rate environment, enhanced annuities and retail distribution review & platforms

- General Insurance (GI) Risk

- impact of the low-interest rate environment, inadequate reserving, UK flooding and periodic payment orders

- Technology Risk

- cyber attacks

- Stakeholder Risk

- Black Swan Risks

- combined effect of financial, catastrophe & pandemic

- Life Products Risk

Note: The low-interest rate environment is a key concern for life insurers because:

- Their assets and liabilities are heavily exposed to interest rate movements.

- In particular, their investments are concentrated in fixed-income securities that return interest, largely bonds.

- Moreover, their liabilities also are sensitive to interest rates.

- Specifically, many of their products, such as annuities, have a guaranteed rate of return, usually in the form of interest that is credited.

- Life insurers’ earnings are mostly derived from the spread between their investment returns, which are mostly interest, and what they credit as interest on these consumer products.

- During times of persistently low interest rates, the spread between interest earned and interest credited is compressed, which not only reduces net income for the insurer but also puts them at risk of being unable to meet contractually guaranteed obligations to policyholders.

Insurance companies hold a diverse range of assets to meet their financial obligations and ensure long-term solvency. These assets generally fall into two main categories:

1. Investment Assets:

They offer potentially high returns but also present unique risks and require careful due diligence.

- Fixed-income securities:

- These are the most common type of asset, including government bonds, corporate bonds, and other debt instruments.

- They offer relatively stable returns and low risk, making them suitable for meeting liabilities with fixed maturities like life insurance payouts.

- Equities:

- Stocks represent ownership in companies and generally offer higher potential returns but also come with higher volatility.

- Some insurers may invest in equities to achieve higher long-term returns, but they do so strategically to manage risk.

- Real estate:

- Investing in properties can provide stable income through rent collection and potential for capital appreciation.

- While offering diversification, real estate investments require specialised expertise and are subject to market fluctuations.

- Alternative investments:

- This category includes assets like private equity, infrastructure projects, and hedge funds.

2. Liquidity Assets:

- Cash and cash equivalents:

- Holding readily available cash ensures the ability to meet immediate claims and operational expenses.

- These typically offer low returns but high liquidity.

- Short-term securities:

- Similar to fixed-income investments, but with shorter maturities (less than a year), offering slightly higher returns than cash with moderate liquidity.

3. Specific Asset Allocation Varies:

The ideal mix of these assets depends on various factors, including:

- Type of insurance: Life insurers have different solvency requirements and risk profiles compared to property and casualty insurers, influencing their asset allocation.

- Liabilities: The timing and size of future payouts impact the need for matching assets with predictable cash flows.

- Risk tolerance: Each insurer balances risks and returns based on their specific risk appetite and business strategy.

Two Financial Risks

Financial risks – Credit and counterparties

| Risk | Impact | Risk Mitigation |

| – Growth of the annuity market poses a significant increase in risk to life insurers. – Particular issue – backing annuities by moving into alternative assets. | A number of annuity writers are backing their liabilities with equity-release mortgages or other non-standard asset classes, which may be unsustainable in the long term. | – Ensure asset classes being considered are fully understood. – Seek permission from the regulator, where necessary. – Actively monitor portfolios for different and unexpected risks. |

Financial risks – Low-interest rate environment impact

| Risk | Impact | Risk Mitigation |

| – The impact of low interest rate environment depends on the extent to which life insurers are asset and liability mismatched. – Margins for assets being managed may be hit as investment returns and profits are reduced. | – Depends on the structure of the portfolio. – Life insurers typically have high bond allocations. – Interest risk hedging activities could put pressure on bond yields causing: • reduction in firm’s solvency levels; • restricted investment policies; • restricted ability to write new business; • reduced new business profitability. • future – may affect the availability of own funds after the effect of subsidiaries to the group under the Solvency II group solvency calculations framework | Ensure there is • appropriate assessment of risk; and • conduct stress testing exercises. • strategy planning should assess vulnerabilities including second-order and behavioural effects and amplification issues. |

Product Risks – Enhanced annuities

| Risk | Impact | Risk Mitigation |

| Enhanced annuities and other non-standard annuities offer higher annuity rates to people whose lifestyle or medical conditions cause their life expectancy to fall below the expected mortality rates | – Low yield environment and difficult macroeconomic conditions mean people are incentivised to derive more value from their savings. – They may be more use of non-standard products against a backdrop of falling standard annuity rates | – Monitor medical advancements affecting future life expectancy that annuities have been provided for. – Ensure books of business do not grow unsustainably. – Ensure credible contingency plans are in place for the treatment of assets for Solvency II. – Firms may wish to consider stress testing their portfolios for scenarios such as withdrawal and/or reduction of reinsurance covers or significant market valuations changes in the future. |

Product risk – Platforms and Retail Distribution Review

| Risk | Impact | Risk Mitigation |

| Retail Distribution Review implemented in December 2012. A fundamental change to the distribution of retail investments could affect consumer behaviour, preference and changes in products and markets attractive to firms. | Back books (consists of old policies that remain on the books as premium-paying policies) steadily declining as maturities and surrenders exceed new business premiums. The key risk – life insurers’ existing books of business decline significantly faster than expected across the sector before new strategies are developed and providing steady cash flow. | Immediate risk of failure is low. Monitoring is required to ensure sector trends of a persistent decreasing back book do not accelerate faster than expected significantly increasing the impact. |

Note on Back books steadily declining

- This decline is due to:

- Policy maturing: Reaching the end of their term and paying out benefits.

- Policyholders surrendering: Cancelling their policies before maturity, often resulting in reduced payouts.

- No new business: These policies are not being replaced with new ones with higher premiums.

Significance of Decline:

- The key risk lies in the faster-than-expected decline exceeding the life insurer’s ability to adapt.

- This can lead to:

- Reduced cash flow: Lower overall premium income can impact the insurer’s ability to meet financial obligations.

- Higher expenses: Maintaining reserves for existing policies while facing declining income can strain resources.

- Profitability issues: Difficulty generating profits if costs exceed income.

Strategies to Mitigate Risk:

- Developing new products: Launching updated policies with higher premiums to replace maturing ones.

- Optimizing existing business: Retaining existing policyholders through better customer service and competitive offerings.

- Risk management: Managing assets and liabilities strategically to ensure solvency and profitability despite a smaller book of business.

Notes on The Retail Distribution Review (RDR)

It aimed to fundamentally change how retail investment products are sold to consumers. It introduced several key changes that could impact consumer behaviour, preferences, and product offerings:

Key Changes:

- Abolished commission-based payments for financial advisors: Previously, advisors earned commissions on the products they sold, potentially creating an incentive to recommend products based on the commission rather than suitability for the client. RDR replaced commissions with transparent fees paid directly by the client.

- Enhanced advisor qualifications and training: RDR raised the minimum qualification level for financial advisors and required ongoing training to ensure they possess the necessary knowledge and skills to provide competent advice.

- Focus on client suitability: Advisors are now required to conduct thorough assessments of the client’s needs, risk tolerance, and investment goals before recommending any product. This shift emphasizes personalized advice tailored to individual circumstances.

- Increased transparency and cost disclosure: Consumers receive clearer information about fees, charges, and potential risks associated with different investment options.

Potential Impact:

- Consumer behavior: Consumers may become more engaged in their investment decisions as they directly pay for advice and have access to clearer information. This could lead to increased demand for personalized advice and greater scrutiny of product features and costs.

- Consumer preferences: Consumers may seek out advisors with specialized expertise aligned with their specific needs and investment goals. This could lead to a shift towards fee-based advisors focusing on long-term wealth management rather than transactional sales.

- Product and market attractiveness: Firms may need to adapt their product offerings to become more competitive in a fee-based environment. This could lead to an increased focus on low-cost index funds, passive investing strategies, and products with transparent fee structures.

Financial risks – Low interest rate environment impact

| Risk | Impact | Risk Mitigation |

| – Slow economic recovery places pressure on premiums, contracting market size, and lowering investment returns which affects profitability. -These factors combined with competition, may result in general insurance firms to seek out more reward for their risk. | – Firms seeking to improve returns may attract significant asset risks to their balance sheet. – Unprofitable underwriting (issuing policies at premiums to attract customers in short-term that don’t adequately cover potential future claims) => can result in firms launching new products writing new and/or growing the business in current and new territories with a lack of data, knowledge or experience. | Continue to focus on: •future underwriting strategies •pricing policies and •monitoring investment strategies. |

Line of business risk – Inadequate reserving

| Risk | Impact | Risk Mitigation |

| Inadequate reserving by general insurers can: •understate the costs of claims; •create premium rate pricing adequacies; and •stress reserving risk capital requirements. | Inadequate reserving will strain business models and affect solvency capital levels. Coupled with: •competitive market pricing pressure; •changing supply and demand trends; •increased claims inflation costs; and •current low interest rate environment can result in pressure to alter an insurers behaviour in the current phase of the underwriting cycle. | Perform regular deep-dive reserve exercises to ensure that they understand their claim exposure fully. Effective reserve governance is essential. Ensure reserves are adequate by using correct booking of reserves with appropriate challenge. |

General Insurance line of business risk – UK flooding

| Risk | Impact | Risk Mitigation |

| More than 30 major rivers in the UK that have extensive reach and are currently or were historically, multi-channelled. These rivers represent significant points of increased vulnerability in the river network to increase flooding. Historic underinvestment in flood defenses and changing weather patterns have increased the risk. | More flooding is predicted in the UK and rates of river bed, bank erosion and floodplain sedimentation are also likely to accelerate. There remains the possibility that certain households will not be able to afford flood insurance as it becomes too costly. | Identify vulnerable points within their insured portfolio of household properties and maintain adequate reserves to manage these exposures. A new regime coming in mid 2015 is intended to ensure the continued widespread availability of flood insurance to high-risk households. Follows the expiry of the Statement of Principles. |

General Insurance line of business risk – Periodic Payment Orders (PPOs)

| Risk | Impact | Risk Mitigation |

| – Since their introduction through the 2003 Courts Act, – PPOs have begun to change the landscape of how large bodily injury (BI) claims are paid in the UK. – PPOs are an alternative to lump sum payments. – Under a PPO settlement an insurer pays a semi-annual amount to the claimant for the remainder of their life, like an annuity. | – This payment method transfers to the insurer risks such as longevity, investment and inflation. – PPOs now pose a material current and future risk for motor insurers. – It is estimated that, within a decade, 25% of general insurer motor reserves could be formed of PPO commitments. | It is essential for: • Firms to actively track and monitor potential PPO claims. • Have specific reserving, modelling and methodology in place to minimise the longevity, investment and inflation risk. |

Technology risk – Cyberattacks

| Risk | Impact | Risk Mitigation |

| Many firms are leaner so are opting to use cloud computing, offshoring data and processes to third party firms. Critical functions outsourced include catastrophe modelling, actuarial analysis and compliance functions. | – A cyber attack could affect a firm’s ability to process premiums and issue insurance contracts affecting cashflows and covers – particularly an issue for compulsory insurances. – A cloud service provider concentration could become a second order risk if such providers were subject to multiple cyber-attacks causing a failure of services. | Ensure and monitor that third party firms provide the security and service that they are contracted to deliver. Constantly monitor firewalls. Rectify breaches immediately to minimise security risks is paramount. Limit staff use of mobile devices to minimise damage to high risk critical areas of the infrastructure. |

Stakeholder risk – Shadow banking activities

| Risk | Impact | Risk Mitigation |

| – Shadow banking activities can cover non-banking financial firms that provide services similar to traditional commercial banks where there is a maturity transformation. – Such activities could include credit investment vehicles (e.g. investment funds, mutual funds and trusts) that have a cash management or very low risk investment objective. – Investments may also occur in unregulated markets, so are not visible in conventional balance sheets, making it difficult to assess exposures. | – Non-traded assets are highly risky and volatile and may cause significant losses in a short timeframe. – They may also be less liquid in times of stress and valuations may be difficult to quantify. | – Firms engage with the regulator to ensure products are appropriate. – Once deemed appropriate firms may require expert advise when transacting in these products. – Firms should regularly monitor asset exposures to minimise risk and volatility. |

Black Swan – Combined effect of a financial, catastrophe & pandemic events

| Risk | Impact | Risk Mitigation |

| Simultaneous shocks to the: •global economic system •natural catastrophes •pandemics could trigger insured loss events which could test the resilience of insurers. | – Certain scenarios could lead to loss in a large number of life products and GI lines of business. – Life and health assurers will be adversely affected in a pandemic event and GI insurers could experience unprecedented liability claims and an accumulation or large value claims following a catastrophe event. – Claims could also come from secondary impacts to society. – A firms solvency capital could be adversely affected if there is a “flight to quality” at the same time due to investor unpredictability. | – Some policies may be hit unexpectedly by claims, the insurance industry should clarify coverage intentions sooner rather than later to ensure contract certainty. – Firms ensure they have an understanding of the financial markets second order, behavioural and amplification issues affecting their investments -Firms ensure they understand their concentration of exposures for natural catastrophe (for modelled and unmodelled perils) – Pandemic contingency plans should aim to ensure continuity of essential operations during an extended period of high illness rates in the workforce, suppliers, and customers. |

Source: Andrea French, Technical Specialist, Insurance Sector Team, the PRA

- Solvency II is an European Union Directive which came into operation in 2016.

- Solvency II sets out requirements applicable to insurance and reinsurance companies in the EU with the aim to ensure the adequate protection of policyholders and beneficiaries.

- Solvency II has a risk-based approach that enables to assess the “overall solvency” of insurance and reinsurance undertakings through quantitative and qualitative measures.

- The regime has been ‘onshored’ as part of the UK’s preparations to leave the EU

- the relevant legislation has been brought into UK law,

- legal changes have been made to ensure that Solvency II reflects the circumstances of the UK’s withdrawal from the EU

- will continue to apply effectively in the UK after the end of the transition period that is, from 1 January 2021.

- Solvency II provides for a market consistent calculation of insurance liabilities and risk-based calculation of capital. It also sets out the supervisory review process and reporting and transparency requirements for insurance firms.

- https://www.bankofengland.co.uk/prudential-regulation/key-initiatives/solvency-ii

- PRA’s proposals to deliver significant reforms for Solvency II, which the PRA considers will lead to a more competitive and dynamic insurance sector in the UK, while maintaining high standards of policyholder protection

- Proposal for Changes and its Potential Impact for Small Insurers

- An increase to the size thresholds at which small insurers are required to enter the Solvency II regime, to increase proportionality for smaller or newer insurance firms. This proposal would benefit small insurers that may be close to the current thresholds, either now or in the future.

- A simpler IM application process, a reduction in reporting costs for firms, and a more proportionate regime for smaller insurers via increased thresholds.

- (IM): A new, streamlined set of rules for internal models (IM) where these are used by insurers to calculate their capital requirements

- The proposal to remove the FRR test would potentially lead to a one-off increase in own funds for a small number of firms, but the effect is not expected to be material.

- Giving small firms more room to grow before being required to comply with Solvency II requirements which may also help them to compete more effectively in UK insurance markets.

See page 14 (consultation paper (CP))

Solvency II supervision involves a two-tiered approach with two main organizations playing key roles:

1. National Supervisory Authorities (NSAs):

- Primary responsibility: Each European Union (EU) member state has its own National Supervisory Authority (NSA). These NSAs hold the primary responsibility for supervising and enforcing Solvency II within their respective jurisdictions. This includes:

- Assessing individual insurance and reinsurance companies’ compliance with the regulations.

- Conducting risk assessments and requiring corrective actions if necessary.

- Granting and withdrawing licenses.

- Investigating potential breaches and imposing sanctions.

2. European Insurance and Occupational Pensions Authority (EIOPA):

- The European Insurance and Occupational Pensions Authority (EIOPA) is a European Union financial regulatory institution.

- EIOPA acts as the central oversight body for Solvency II implementation across the EU.

- Its main functions include:

- Developing implementing technical standards and guidelines to clarify and supplement the Solvency II Directive.

- Promoting consistent supervisory practices among NSAs through peer reviews and guidance.

- Mediating disputes between NSAs regarding supervisory decisions.

- Conducting stress tests and risk assessments at the EU level.

- Websites

- Smaller Insurers Webpages

- http://www.bankofengland.co.uk/pra/Pages/supervision/smallinsurers/default.aspx

- Solvency II webpages on Bank of England website

- www.bankofengland.co.uk/Solvency2

- European Commission website

- http://ec.europa.eu/internal_market/insurance/solvency/index_en.htm

- EIOPA website

- https://eiopa.europa.eu/

- The PRA’s approach to supervising liquidity and funding risks: https://www.bankofengland.co.uk/-/media/boe/files/prudential-regulation/supervisory-statement/2021/ss2415-jan-2022.pdf

- Strategic objective

- ensuring the relevant markets function well

- Operational objectives

- promoting effective competition in the interests of consumers;

- securing an appropriate degree of protection for consumers; and

- protecting and enhancing the integrity of the UK financial system.

- FCA Statutory Objectives

- Securing an appropriate degree of protection for consumers

- Promoting effective competition in the interests of consumers:

- the needs of different consumers

- the ease with which consumers can change providers

- the ease of new entry

- how far the competition is encouraging innovation

- Protecting and enhancing the integrity of the UK financial system (including)

- soundness, stability and resilience

- orderly operation of markets

- financial crime

- market abuse

- transparency of price formation

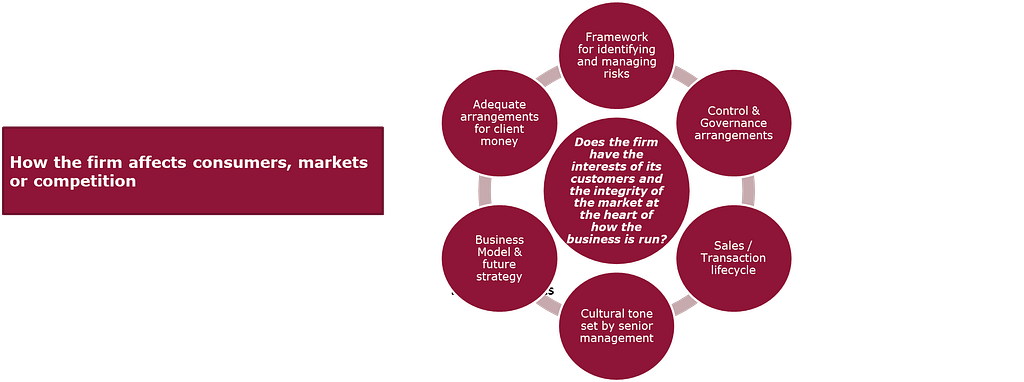

- Aim of Supervision

- To ensure firms have the interests of their customers and the integrity of the market at the heart of how they run their business.

- How will FCA do this?

- By influencing, persuading and, where appropriate, using formal powers to achieve a significant transformation in firms’ conduct behaviours.

- For what population of firms?

- The FCA is responsible for the retail and wholesale conduct supervision of c.25,000 firms

- The FCA is also responsible for the prudential supervision of c.23,000 firms (i.e. those that are not prudentially regulated by the PRA).

Although primarily a conduct regulator, the FCA is the sole regulator for firms not prudentially regulated by the PRA.

| The FCA’s Approach | Key Features |

| •Starting principle is that firms should be allowed to fail, therefore, the focus is on mitigating the impact on retail customers and market integrity of firms failing or under financial strain. •This approach is to ensure that any failure is orderly by ensuring that customers assets and money are protected. •Prudential supervision is graduated according to prudential significance. •On-going dialogue with PRA where we both have prudential responsibilities for a group. | Prudential Classification – based on the impact that the disorderly failure of a firm could cause in terms of market disruption and market failure. Setting Capital & Liquidity Financial Resource Requirements – assessing financial resources requirements for the most prudentially significant firms. Regulatory Return Monitoring – pro-actively reviewing returns for the most significant firms and acting on alerts for other firms. Thematic Work – cross-firm capital / liquidity work (including smaller firms) |

The FCA aims to be a judgement based, forward-looking and pre-emptive regulator

The FCA’s approach emphasises 5 elements:

- be forward-looking in the assessment of potential problems – looking at how we can tackle issues before they start to go wrong;

- intervene earlier when we see problems and before they cause consumer detriment or damage to market integrity;

- tackle underlying causes of problems, not just the symptoms, as this will be more effective and efficient in the long term for consumers and firms;

- secure redress for consumers if failures do occur; and

- take meaningful action (credible deterrence) against firms that fail to meet our standards, including levels of fines that have a deterrent effect.

To do this, in addition to the powers inherited from the FSA, they are able to:

- Temporarily ban products or restrict sales for up to 12 months;

- Stop misleading financial advertising;

- Impose requirements on firms; and

- Subject to consultation, tell the market earlier about enforcement action.

How will FCA achieve their objectives?

Firm Systematic Framework – Key judgements

- The FCA and PRA operate under different sets of objectives, although there is a Memorandum of Understanding in place between the two setting minimum co-ordination standards, including:

- Domestic supervisory colleges, with the frequency depending on the categorisation of the firm;

- Regular exchange of information, including material conduct risks, internal models, and capital and liquidity requirements (e.g. coverage of conduct risks in ORSA-Own Risk and Solvency Assessment);

- Notification of findings of Pillar 3 work

- Pillar 3 requires firms to publicly disclose information relating to their risks, capital adequacy, and policies for managing risk with the aim of promoting market discipline.

- Consultation on SIF (an FCA Significant Influence Function) applications;

- Expressing independent views on Part VII transfers; and

- Specific requirements for with-profit businesses.

- The supervisory teams will strive to coordinate where possible.

- The FCA’s statutory objective is to secure an appropriate degree of protection for consumers.

- Customers do not always behave rationally and firms can exploit consumer biases.

- The FCA is using Behavioural Economics (eg. randomised control trials) to better understand these and inform our supervisory approach.

- Evidence of how their consumers receive appropriate outcomes, throughout the product lifecycle

- Implement targets that are aligned with consumers’ actual cover requirements

- Understand the difference between customers being satisfied and customers being treated fairly

- Identify, capture and mitigate the risks to their customers receiving inappropriate outcomes

- The FCA’s focus is to ensure the integrity and resilience of wholesale/commercial insurance markets, rather than seeking to introduce concepts of detriment and redress that we use in retail markets.

- Firms should recognise, however, that activities in retail and commercial markets are interconnected and that risks caused by poor conduct can be transmitted and undermine both markets.

- The FCA places more emphasis (and takes a more assertive and interventionist approach) in particular on three areas:

- where commercial products filter down or are distributed to retail consumers;

- where certain behaviours in commercial markets can cause damage to market integrity; and

- where market structures can result in participants being disadvantaged or the market being inefficient.